The Australian S&P/ASX 200 Index finished the week up 1%, with small companies outperforming large companies with the Small Ordinaries Index rising 1.8%. Materials were the best performing sector (+4.5%). Information Technology (-3%) was the worst-performing, led by a 12.2% fall in Afterpay (APT) after the announcement of Apple (AAPL) entering the Buy Now Pay Later space.

In the US, the S&P 500 closed 1% lower. The tech-focused NASDAQ Composite fell 1.87%, with investors concerned by a CPI Inflation reading that showed an increase of consumer prices of 5.4% from June 2020, the fastest pace in nearly 13 years. This significant jump was primarily attributed to new and used cars, airfares, hotel rooms and gasoline prices, all linked to the reopening of the economy and considered transitory. However, some price rises may prove to be stickier, including rent and the cost of dining out. These inflation readings will remain the main narrative in the markets over the coming months, as investors closely scrutinise whether inflation is here to stay.

Australian economic news remains supportive of equity markets. Australian employment exceeded expectations in June despite lockdowns in various states, with unemployment falling to 4.9% and 51,600 full-time jobs added. The Westpac-Melbourne Institute Index of consumer confidence rose 1.5% to 108.8. However, this was before the announcement of tightening lockdown restrictions in NSW.

In company news, Pendal (PDL) reported solid inflows into their higher-margin equity and fixed income products of $1.2B. Outflows from lower margin cash products equalled $1.9B, leading to overall net outflows. We believe the strength of inflows in their US funds management business and ESG funds, bodes well for continued growth in funds under management and associated performance fees.

Woodside Petroleum (WPL) provided a second-quarter report with results within market expectations. We were expecting the cost of development to increase given higher commodity, construction and labour prices. There remains a list of positive catalysts in the near term that could see the stock re-rate upwards.

Rio Tinto (RIO) 2Q21 production fell 9% due to heavy rainfall, processing plant availability, a tight labour market, and their costs rose in further news. Management stated that production would be at the lower end of full-year guidance. While disappointing, the company continues to benefit from historically high iron ore prices.

Sydney Airport (SYD) rejected the recent takeover bid calling it opportunistic. Spark Infrastructure (SKI) also received a takeover offer, led by KKR, showing investor demand for infrastructure assets continues unabated. Wesfarmers (WES) bid to acquire Australian Pharmaceutical Industries (API), the owner of Priceline. Early indications are that they will have to increase the price offered to get the deal across the line.

For the week ahead, investors will be analysing the RBA latest minutes, the European Central Banks interest rate decision and associated commentary, and preliminary PMIs for most major economies.

US Earnings Preview

US 2Q21 earnings season kicked off last week, with 41 companies in the SP500 have reported to date, and over 90% have reported earnings above analyst estimates. This compares favourably to historical averages, as does the margin of the beat, demonstrating the strength of the US economic recovery.

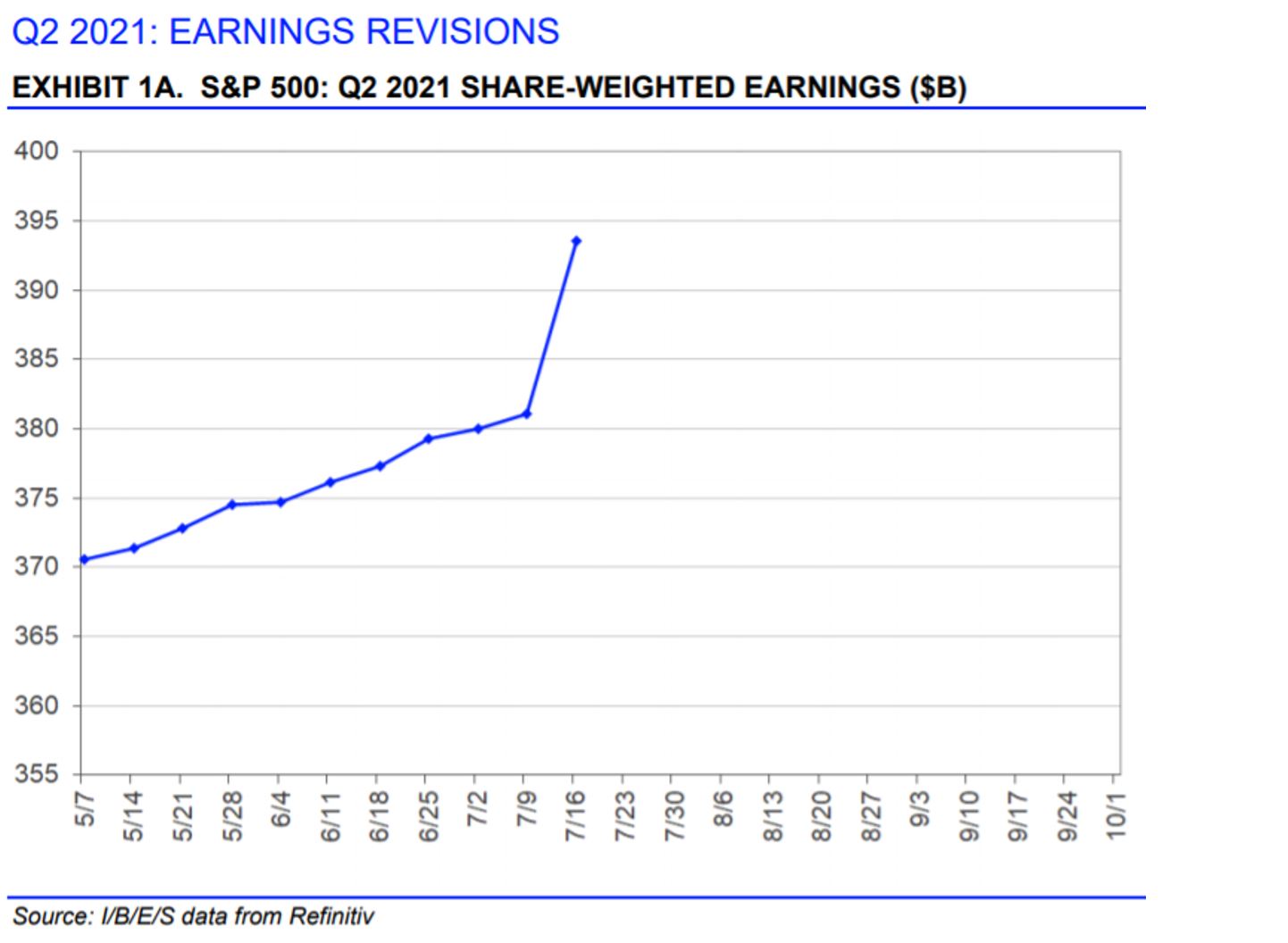

Aggregate Q2 2021 S&P Earnings expectations have continued to rise in light of these robust reports.

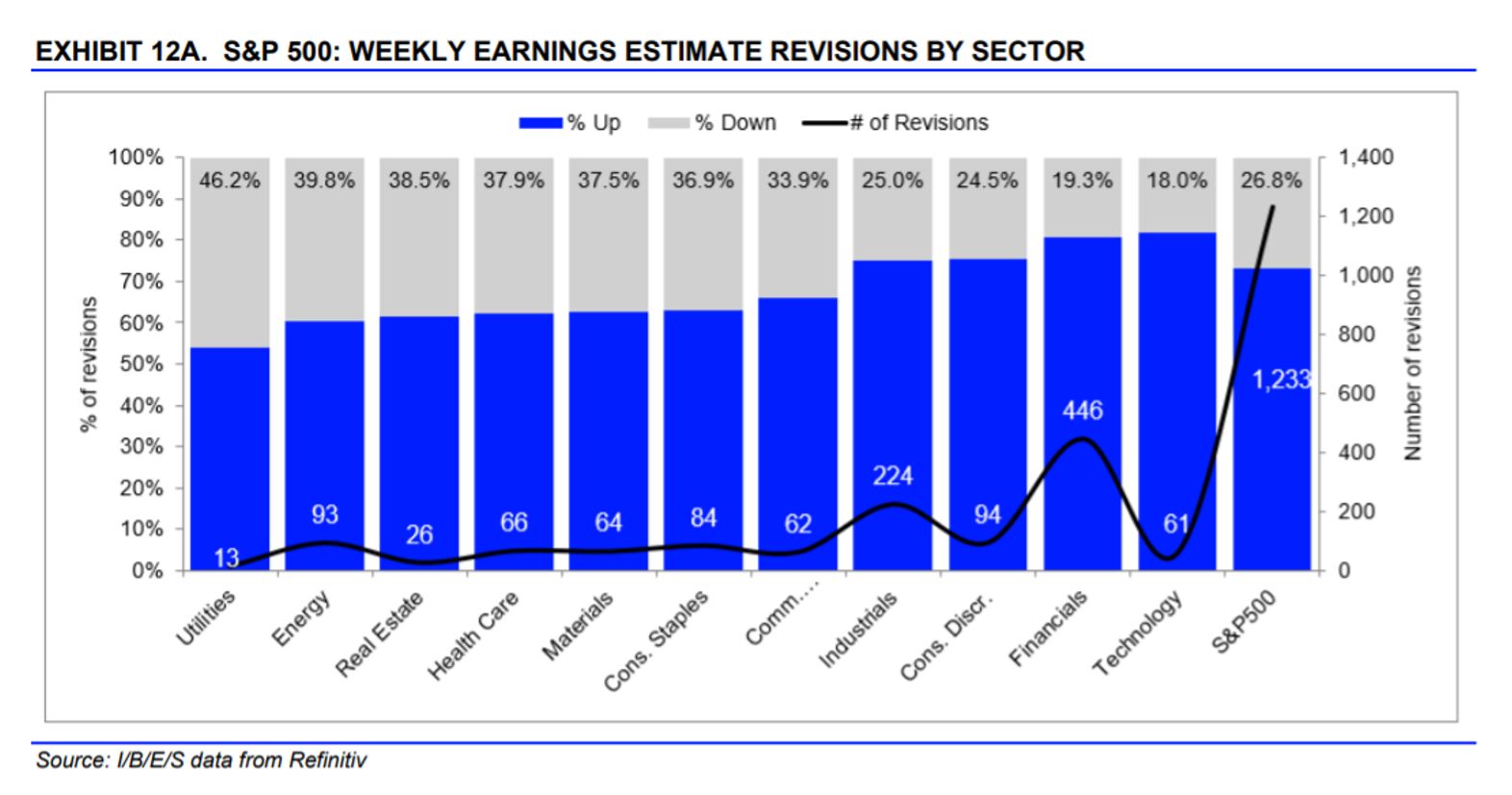

The second-quarter earnings season picks up this week, with reports from companies including Netflix, Coca Cola, Johnson & Johnson, Twitter, AT&T and Intel. As shown in the chart below, Technology is the sector with the highest percentage of positive analyst revisions.

With the S&P 500 up roughly 15 per cent so far this year, investors will look for solid company forecasts and management commentary to justify prevailing high valuations. If earnings continue to beat analyst estimates over the coming weeks, and by historically significant margins, the US stock market could well continue to rise over the near term as companies grow into their lofty valuations.

–

Monday 19 July 2021, 5pm

For more information on the above please contact Bentleys Wealth Advisors directly or on +61 2 9220 0700.

This information is general in nature and is provided by Bentleys Wealth Advisors. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decision based on this information.