From Jonathan Bayes, consultant Chief Investment Officer, Bentleys Wealth Advisors

Economic data released

U.S employment figures surprised strongly in November rising a whopping 266,000 for the month and taking the U.S unemployment rate to its equal lowest level since the 1950’s. The figure was a surprise given other data points to a slowing in job openings. Further encouragement in U.S data last week came from the Michigan Consumer Sentiment release for December which also showed a jump following recent weakness.

Australian Service sector activity continued to improve in November and the new order index encouragingly jumped to its highest level since mid-2018, providing us with a degree of confidence that local consumption was trying to bottom out.

Australian construction sector activity however remains subdued in November, with residential activity weak but stabilising, but perhaps more concerningly, new orders for engineering and commercial construction activity falling to 6 to 7-year lows.

We address the softening in non-residential construction below.

Observations from the past week

Afterpay (APT) shares ended the week down -5%, and still around -20% lower than their all-time highs made in September.

This is in spite of again another blockbuster trading update in which the group confirmed November had seen a record $1bn in underlying sales and a staggering 500,000 new users to the platform.

Almost exclusively this growth was in the newer American and British markets, with the U.S business now the same size as the Australian/New Zealand operation within only 18 months of launch.

Remember of course that only a month ago, APT signed a deal to partner in providing ‘buy now, pay later’ services to Ebay’s Australian merchant base in calendar 2020 in a move that has the potential to double the number of merchants on the APT platform locally.

On top of that, the group conducted a $200m private placement to well-regarded technology investor Coatue Management at $28.50 to facilitate the expansion of APT services into new markets.

There is still plenty of road to run on APT and it would surprise us if the share didn’t breach $40 during 2020.

Remains a key and core Australian equity position.

Boral (BLD) shares were disappointing last week, falling -10% after they announced the discovery of financial irregularities within their North American windows division.

Whilst its unknown if the initial $44m cost impost will be the end of it, the announcement just adds to investor discomfort with BLD, their North American acquisitions and the CEO Mike Kane who made these deals.

The Windows acquisition was made by Headwaters before BLD acquired the Headwaters fly-ash operation, the latter having failed to hit internal targets in every year since acquisition.

U.S housing markets are booming right now, but BLD continues to get stuck in the mud, which has proven a material frustration to domestic Australian investors.

We suggest investors await further clarity on the situation, however we do believe BLD shares look attractive in the medium term at current levels.

What’s interesting?

We have had the view in recent months that we would see the Australian household emerge from its post-Federal Election slump in 2020 with increased vim and vigour as the combined impacts of multiple stimuli and rising house prices helped Australian households to see the brighter side of life.

Further compounding this glass half full attitude to the domestic economy was our belief that the Federal Government would bring forward significant personal income cuts from their 2022-2024 schedule, perhaps as early as the coming 2021 financial year.

We still feel this is likely, but we would be remiss not to address the dramatic slowing seen beyond residential construction in the engineering and commercial construction spheres over the last 6 months.

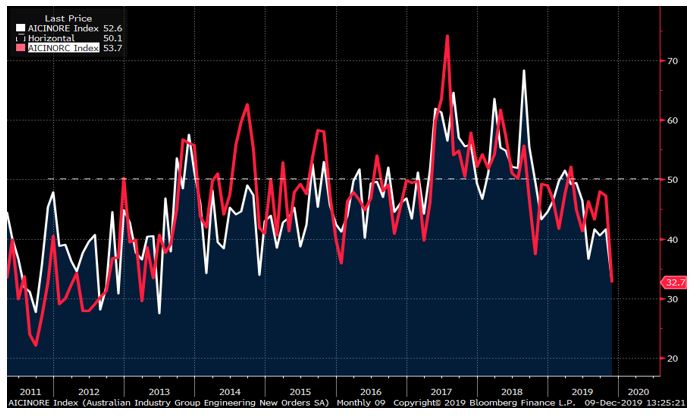

The chart below shows new order momentum in engineering (white) and commercial (red) construction according to the monthly Australian Industry Group Construction data released on Friday.

Numbers above 50 represent improving conditions on the prior month and numbers below the opposite.

You can see from the chart that the fall below 50 has only worsened, making the deterioration on a month on month basis through the 2H of 2019 all the more concerning.

The government needs to nip this in the bud sooner than the May Federal Budget proclamation or we risk 2020 being a lost year for growth, and my willingness to embrace a more optimistic economic narrative a forlorn hope.

One to watch.

Worrying deterioration in Australian non-residential construction activity

Looking ahead

- Monday – CH Monetary Aggregates – new loans, money supply etc (Nov)

- Tuesday – AU NAB Business Confidence (Nov), AU House Price Index (Q3), US NFIB Small Business Confidence (Nov)

- Wednesday – AU Westpac Consumer Confidence (Dec), US Federal Reserve (Thu morning AEST), US CPI (Nov)

- Thursday – AU Retail Sales (Oct), AU Westpac (WBC) AGM, UK National Election

- Friday – AU Pendal (PDL) AGM

Beyond the economic data and AGM’s this week, the US Federal Reserve meeting Thursday morning AEST and the UK Election on Thursday night AEST will clearly gain some attention.

However, of more importance will be the Sunday December 15th due date for the United States to add 15% tariffs to a further $150 billion of Chinese-produced goods bound for the United States

Friday 5pm values

| Index | Change | % | |

| All Ordinaries | 6813 | -134 | -1.9% |

| S&P / ASX 200 | 6707 | -138 | -2.0% |

| Property Trust Index | 1642 | -25 | -1.5% |

| Utilities Index | 8002 | -156 | -1.9% |

| Financials Index | 5961 | -113 | -1.9% |

| Materials Index | 13355 | -254 | -1.9% |

| Energy Index | 11410 | -267 | -2.3% |

Friday Closing Values

| Index | Change | % | |

| U.S. S&P 500 | 3146 | +6 | +0.2% |

| London’s FTSE | 7240 | -106 | -1.4% |

| Japan’s Nikkei | 23354 | +61 | +0.3% |

| Hang Seng | 26498 | +152 | +0.6% |

| China’s Shanghai | 2912 | +40 | +1.4% |

Key Dividends

| Mon 9th December 2019 | Div Ex-Date – WBCPI

Div Pay Date – MXT, MOT |

| Tue 10th December 2019 | Div Pay Date – MQGPD |

| Wed 11th December 2019 | Div Ex-Date – ANZPG, ANZPH, NABPE |

| Thu 12th December 2019 | AGM – Westpac (WBC)

Div Ex-Date – NABPC, WBCPE, WBCPF, WBCPH Div Pay-Date – NAB (NAB), RESMED (RMD) |

| Fri 13th December 2019 | AGM – Pendal (PDL) |

Tuesday 10 December 2019, 2pm

For more information on the above please contact Bentleys Wealth Advisors directly or on +61 2 9220 0700.

This information is general in nature and is provided by Bentleys Wealth Advisors. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decisions based on this information.