Tech…again

Volatility was once again the flavour of the week.

With US markets closed on Monday for the Labor Day holiday one could be forgiven for thinking price action may have been somewhat muted. However, this quickly proved to be anything but the case with equity markets clearly devoid of any strong direction posting gains one day and losses the next.

US tech stocks once again drove the market lower.

The NASDAQ fell -4% on Tuesday, rallied nearly +3% on Wednesday before fading a further -2% on Thursday and Friday.

Much of this weakness can again be traced back to the FAANG stocks which continue to see profit-taking.

Facebook (FB), Amazon (AMZN), Apple (AAPL), Netflix (NFLX) and Google (GOOG) all fell between -4% and -7%.

Tesla (TSLA) which last week saw its shares surge +20% on the back of a stock split and $5bn share sale fell -10% after the electric-vehicle maker missed out on being included in the S&P 500 Index. Investors had assumed its inclusion in the benchmark would generate significant inflows from passive investments with those who purchased stock now having to wait until the TSLA ‘Battery Day’ on September 22 for the next positive catalyst.

The ongoing arm wrestle between investors trying to gain exposure to high quality tech stocks and traders using some of these sharp rallies to take profit continues to underpin this lack of conviction.

US inflationary data released on Friday came in higher than expected with the Consumer Price Index (CPI) rising +1.3% on a one-year view, an increase from +1.0% in July. Core inflation which strips out volatile costs such as fuel rose to +1.7% benefitting from the gradual reopening of the US economy.

Despite the uptick Federal Reserve policy makers see little threat to inflation overshooting with the Federal Reserve meeting this week set to hold interest rates steady.

Elsewhere, oil prices fell -6% after US crude stockpiles rose 2 million barrels last week on the back of six consecutive weeks of declines. Concerns over China’s capacity to continue purchasing record amounts of crude and Saudi Arabia’s intention to reduce pricing saw oil prices fall to near three-month lows.

Rising stockpiles and stalling demand will be the major focus when the market monitoring panel of the Organisation of the Petroleum Exporting Countries (OPEC) meet later this week.

We currently have no exposure to oils in our portfolios having sold Oil Search (OSH) in April this year as coronavirus lockdowns impacted demand for oil from both the automobile and airline industries.

More stimulus on hold

On Thursday Senate Democrats blocked the $300bn Republican coronavirus stimulus package.

Whilst not unexpected, given the Democrats had previously sought a $3 trillion bill, the outcome weighed negatively on markets with the S&P 500 falling -2.5% for the week.

With the stimulus package failing there remains little hope of Congress passing a relief deal before November’s election which is cause for concern.

The high number of Americans filing new claims for unemployment benefits indicate that the recent labour market recovery is losing momentum with 884,000 workers filing for unemployment compensation last week and claims from individuals filing for at least two weeks increasing to 13.3 million.

Brexit Treaty Breakdown

The GBP was the worst performing major currency last week falling -3.6% against the USD and AUD on the back of rising tensions between the UK and the EU.

UK PM Boris Johnson’s plans to amend part of the Brexit withdrawal agreement reduced confidence in the likelihood of a deal being finalised by October 15 with the EU warning the UK could face legal action for the proposed changes which undermine the treaty signed last year.

A key component of the withdrawal agreement was designed to prevent a hard border returning to Northern Ireland which would allow the UK to modify rules relating to the movement of goods between Britain and Northern Ireland.

Given this is in clear breach of the signed treaty amending the bill will be regarded as a violation of international law and bring further uncertainty to the Brexit deal.

Vaccine worries

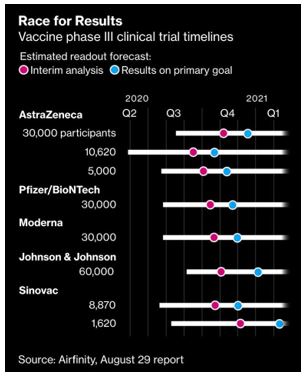

One of the most promising vaccine candidates suffered a hiccup last week as the AstraZeneca phase 3 trial was paused following reports of a potentially serious adverse reaction. The market reaction to the news was mild, with tech stocks strengthening a little amid the sector’s sell-off while sectors most hurt by lockdowns were slightly lower after holding up well through the previous week’s drawdown. This did not last for long however, as tech resumed its recent correction. Over the weekend, news broke that the phase 3 trial has resumed though futures are indicating little reaction again.

However, this event highlights the potential risks to the vaccine timeline as most expect results within a couple of months and a vaccine by early 2021.

Australia in Review

The ASX fell -1.3% with energy stocks faring worst down -5% impacted by declines in the price of oil.

Australian business conditions weakened sharply in August with NABs business confidence survey highlighting business concerns over hiring.

Forward orders weakened and capacity utilisation edged lower (and remains very low) – and alongside the weak level of confidence, suggest that conditions may deteriorate further.

An improvement in Covid-19 case numbers in Victoria provided some relief with forecasts having been worse, however a deterioration in the employment index suggests that while the economy has begun to open up, the labour market is still weakening.

Westpac consumer confidence numbers presented a similar picture with the index bouncing +18% in September boosted by improving conditions and the absence of a second Covid-19 wave in states other than Victoria.

The rebound means the Index is now just 1.6% below the average over the six months prior to the emergence of COVID-19 in March.

This week central bank news will dominate proceedings with the Bank of Japan, Bank of England and Federal Reserve meetings all set to take place and locally the RBA minutes tomorrow and unemployment data on Thursday.

We remain cautious ahead of the US election in early November as the polls continue to indicate a very tight race. Given the vastly different policies the Republicans and Democrats intend to introduce and the likely impacts these will have on different segments of the market we believe it is prudent to hold cash which we will look to invest once some of the volatility comes out of the market.

Looking ahead

| Monday | EU Industrial Production (AUG) |

| Tuesday | CN Industrial Production (AUG), CN Retail Sales (AUG), US Industrial Production (AUG) |

| Wednesday | AU HIA New Home Sales, US Retail Sales (AUG), US Business Inventories (JUL), US Federal Reserve Statement |

| Thursday | AU Employment Data (AUG), JP Bank of Japan Statement, EU CPI (AUG), US Housing Starts (AUG), US Initial Jobless Claims |

| Friday |

–

Tuesday 15 September 2020, 10am

For more information on the above please contact Bentleys Wealth Advisors directly or on +61 2 9220 0700.

This information is general in nature and is provided by Bentleys Wealth Advisors. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decision based on this information.