From Jonathan Bayes, consultant Chief Investment Officer, Bentleys Wealth Advisors

Key market themes

Update on the coronavirus

- Equity markets are now down on average -10% to -14% from their highs and year-to-date

- The ASX200 is -5% year-to-date, but down -11% inclusive of the Australian Dollar’s fall to a decade low as part of this move

- Global bond markets have continued to rally with Australian and US 10-year yields reaching record lows of 0.7% in Australia on Monday morning and 1.14% in the United States on Friday

- Chinese February economic data has begun being reported and is demonstrating the huge impact felt on economic activity from the quarantine process (see below)

- Globally the virus is spreading to parts of Europe and North and South America which is causing concerns of a wider pandemic

- Investors should follow closely the easing or tightening in travel restrictions between countries and intra-country as a real-time guide on the containment or lack thereof, of the virus

- We are watching daily Tom-Tom traffic congestion data online in major Chinese cities as our guide on the speed with which workers are returning to their jobs

- We would also highlight Google search as a sensible guide to watch the degree of public interest or panic in places like the United States and Europe – type coronavirus into Google Trends to understand the significance of users ‘searching’ for that term

US Politics

- The big focus this week will be on the Super Tuesday Democrat primaries in which 14 states (including the likes of California and Texas) will vote for their nominated candidate

- After Joe Biden’s success in South Carolina, the feeling is that it is down to these two candidates for the nomination and success in Tuesday’s elections has the potential to catapult successor into frontrunner status

Economic data released

Major week for U.S and Australian data post the virus impact

- With the start of March now upon us, our focus and that of investors will be on the release of March economic figures in each of Australia, China and the United States to ascertain the impact on economic activity from the coronavirus

- As the charts on Chinese activity below demonstrate, February was a write-off for Chinese economic activity

- In the United States and Australia it will be less easy to predict, but we will be focused on both the manufacturing and service sector sentiment indices due in each country as well as US employment figures in the United States

Company News

Afterpay (APT) results were exceptional

- Whilst APT shares certainly were heavily sold off last week post Thursday results, there is no denying the franchise strength in the figures released

- Heavier cost investment by the company in expanding its footprint caused analysts to downgrade near term profitability, but raise long term assumptions on turnover, customer numbers and ultimately, group profitability – so this is a timing thing

- It didn’t help that one of its major brokerage supporters, Goldman Sachs, downgraded the stock from BUY to HOLD and removed it from its Conviction Buy list

- The results themselves were incredibly strong in terms of customer metrics and I would suggest that APT be considered in the same vein as Amazon (AMZN) in its willingness to reinvest growth cashflows in building out its global footprint and competitive moat against a growing group of pretenders to the buy-no pay-later crown

- Customer numbers beat expectations in each of its existing markets (3.1m in Australia, 3.6m in the United States and already 600k in the UK) and in total by 10% (7.3m subs vs 6.6m forecast) and sales turnover also beat expectations by 10%

- Frequency of turnover is also increasing, which is a major positive for future sales and comes at significantly higher incremental margins – as a guide

- The company furthermore announced it would roll-out ‘in-store’ in the United States in June and launch in Canada later in 2020

- Having trimmed some of our position at $40, we are well-placed to add to holdings at or near $30 if given the opportunity

Reliance Worldwide (RWC) shares were clubbed -25% after downgrading 2020 profit expectations

- RWC surprised some of us with a downgrade to 2020 cashflow assumptions to $265m-280m in EBITDA (from $280-305m) after having delivered only a small miss for 1H figures

- The group blamed a poor sell-through of new products which failed to cover increased R&D expenses born in new product development

- Group cash flow conversion was excellent and cost synergies from the John Guest acquisition are well on track

- Importantly despite the softness in European end-markets, the European division managed to meet expectations

- Brokers chose to lower earnings numbers by around -10% which is significantly less than the sell-off last week, however investors sold the stock heavily given it had materially outperformed the index in the lead-up and had room to give up

- RWC is now back at our recommended buying levels and now at a modest discount to the ASX200 on 2021 earnings which we think is too low

Observations from the past week

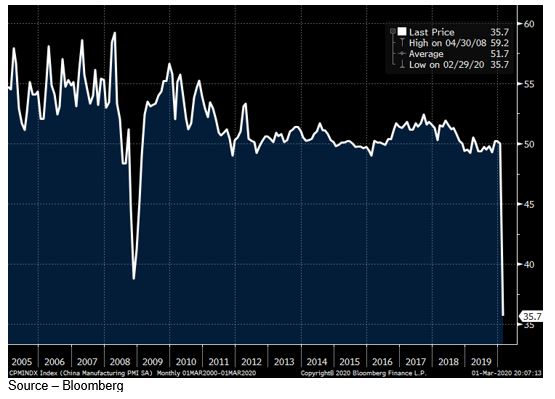

Chinese Manufacturing Sentiment collapses in February

The first economic data out from China for February came out over the weekend, being the government’s official measure of manufacturing activity.

As the chart below shows, the industrial economy stopped in its tracks in February on account of the spread of the corona-virus and measures taken to quarantine its multiplication.

Sentiment last month was worse than at the peak of the GFC.

Even more interesting was that the Chinese government were willing to share a number this negative as its widely taken that this official data measure is smoothed out by the administration – perhaps its seen as an important benchmark to demonstrate to the population the significance of the decline as a means for gauging the hoped-for success in their recovery efforts as 2020 progresses.

Chinese Small-Medium Enterprise Confidence also collapses in February

Similar to the official manufacturing data, the chart below shows the privately compiled Standard Chartered Small Medium Enterprise Confidence Index for February, and it too has collapsed in a hole.

Notably the production, profitability and new order indices bore the brunt of the economic impact, with overall confidence falling significantly into negative (which is <50), but still at a level that suggests respondents feel hopeful that the impact of the virus will be short term in nature (confidence only fell to 40.3).

Looking ahead

| Monday | US Markit Manufacturing PMI (FEB), ISM Manufacturing (FEB), AU AIG Manufacturing Index (FEB), CBA Manufacturing Index (FEB), ANZ Job Advertisements (FEB) |

| Tuesday | AU Building Approvals (JAN), RBA Meeting |

| Wednesday | US ADP Employment (FEB), Markit Services PMI (FEB), ISM Services PMI (FEB), AU AIG Construction Index (FEB), CBA Services Index (FEB), GDP (Q4) |

| Thursday | US Challenger Job Cuts (FEB), Bloomberg Weekly Consumer Confidence (MAR), AU Trade Balance (JAN) |

| Friday | US Employment Report (FEB), AU Retail Sales (JAN), AIG Services Index (FEB) |

Beyond the day-to-day news-flow on corona-virus infections, markets will pay close attention to the outcome of Super Tuesday’s (March 3rd) Democratic primaries in which 14 states (including California and Texas) will vote for their favoured Democrat challenger and virtually 1/3rd of all the delegates to the Democratic National Congress will be decided.

Friday 5pm

| Index | Change | % | |

| All Ordinaries | 6511 | -719 | -9.9% |

| S&P / ASX 200 | 6441 | -698 | -9.8% |

| Property Trust Index | 1579 | -139 | -8.1% |

| Utilities Index | 7832 | -545 | -6.5% |

| Financials Index | 5904 | -590 | -9.1% |

| Materials Index | 12390 | -1485 | -10.7% |

Friday closing values

| Index | Change | % | |

| U.S. S&P 500 | 2954 | -419 | -12.4% |

| London’s FTSE | 6580 | -856 | -11.5% |

| Japan’s Nikkei | 21142 | -2337 | -10.0% |

| Hang Seng | 26129 | -1480 | -5.4% |

| China’s Shanghai | 2880 | -150 | -5.0% |

Key dividends

| Date | |

| Mon 2 March 2020 | Div Ex-Date – Fortescue (FMG), Platinum (PTM), QANTAS (QAN), VGI Partners (VG1)

Div Pay Date – ANZPD |

| Tue 3 March 2020 | Div Ex-Date – AMCOR (AMC), Medibank (MPL), Oil Search (OSH) |

| Wed 4 March 2020 | Div Ex-Date – Woolworths (WOW), Treasury Wine (TWE) Perpetual (PPT), Bingo (BIN) |

| Thu 5 March 2020 | Div Ex-Date – ASX (ASX), BHP (BHP), CBAPE/CBAPF, CBAPD, CBAPG, CBAPH, CBAPI, Pinnacle (PNI), QBE (QBE), Rio Tinto (RIO) |

| Fri 6 March 2020 | Div Ex-Date – Bendigo Bank (BEN), Flexigroup (FXL), NABPF, Wisetech (WTC)

Div Pay Date – JB Hi Fi (JBH) |

Monday 2 March 2020, 4pm

For more information on the above please contact Bentleys Wealth Advisors directly or on +61 2 9220 0700.

This information is general in nature and is provided by Bentleys Wealth Advisors. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decisions based on this information.