From Jonathan Bayes, consultant Chief Investment Officer, Bentleys Wealth Advisors

Market update

We have begun to refer to the current pocket in markets as something like a ‘twilight’ period.

There are several reasons.

Firstly, the run of March, April and May economic data has been so bad that it can only improve as economies slowly re-open.

Secondly, the added support to consumption offered by government benefits such as Jobkeeper has provided much-needed ballast to a struggling economy and ensured that the economic deterioration wasn’t even worse.

Finally, having seen the positive impact of social distancing, infection ‘curves’ have indeed been flattening in major developed countries such as Australia and in large parts of Europe and the United States.

In a relative sense, the needle has shifted to a positive one, albeit like the sword of Damocles, the threat of a re-escalation in infection rates is looming, particularly in certain parts of the United States.

Equally the true economic pain from shelter-in-place orders has been anaesthetised and it won’t be until the end of support programs like Australia’s Jobkeeper (end September) or the Paycheck Protection Program (end July) equivalent in the United States ends that the full toll is revealed.

Hence, investment markets sit in an eerie twilight, hopeful but with significant hurdles ahead.

For those of you interested to track the progressive re-opening of cities, I would direct you to the following websites:

- https://www.tomtom.com/en_gb/traffic-index/melbourne-traffic/

- https://www.apple.com/covid19/mobility

Observations for the past week

Construction activity set to soften considerably

- We have flagged our concerns on domestic construction activity for some time, noting the combined impact of job losses and limitations on net migration levels as a major factor likely to see domestic residential starts slow considerably

- Major building group Fletcher Building (FBU) last week guided to a -15% annualised fall in Australian residential building approvals by the end of the June financial year, a similar -15% fall in commercial activity and a -10% fall in infrastructure activity

- It’s quite likely that at the annualised rate, these figures could worsen as the calendar year drags on

- With the construction sector employing roughly 10% of the Australian work force, the fall in order backlogs is a major threat jobs and economic activity in the near term, which when added to the job losses experienced across retail, food service and tourism sectors (themselves contributing almost 20% of the workforce) is a very dark cloud across the domestic economy, particularly when Jobkeeper supplements end in September

- The chart below shows the monthly residential building approvals for private houses (in red) and the index on new housing orders from the Australian Industry Group (in white) and doesn’t paint a pretty picture

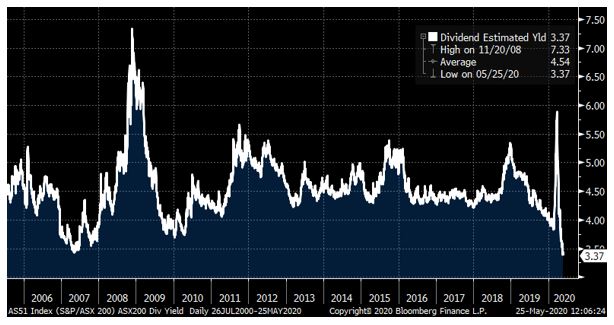

Search for Yield amongst the ASX200

- The chart below shows the forward forecast dividend yield for the ASX200 and how it compares to history

- As can be seen, the dividend yield forecast on the ASX200 has collapsed to its lowest level in decades as companies prioritise balance sheet security over returns to shareholders

- We think its unlikely Australian banks pay second half dividends as 2020 draws on and the impact of job losses mount on their lending books, however we do expect this capital retention will allow banks to resume payments in 2021 at a payout ratio nearer to 50%

- We do however feel very confident on the dividend payment abilities of recent portfolio additions such as Coles (4%+), Spark (6.5%), Invocare (4%+) and from dividend stalwarts such as Telstra (5%+), IOOF (6%+), Pendal (6%) and AMCOR (5%)

- Beyond the Australian equity piece, we do believe listed debt vehicles such as the Qualitas Real Income (QRI) fund and each of the Metrics Master Income (MXT) and Metrics Opportunity Trust (MOT) offer impressive relative income at current discounts to net asset values

Looking ahead

| Monday | US MEMORIAL DAY HOLIDAY |

| Tuesday | AU Weekly ANZ Consumer Confidence, US Chicago Fed National Activity Index (APR),

US Consumer Confidence (MAY), US Dallas Fed Manufacturing Index (MAY) |

| Wednesday | N/A |

| Thursday | AU Private Sector Capex (Q1), US Richmond Fed Manufacturing Index (MAY), US Beige Book report, US GDP (Q1), US Weekly Jobless Claims & Weekly Consumer Confidence |

| Friday | AU Private Sector Credit (APR), US Chicago PMI (MAY) |

A very quiet week with US public holiday Monday restricting activity.

Friday 5pm values

| Index | Change | % | |

| All Ordinaries | 5608 | +116 | +2.0% |

| S&P / ASX 200 | 5497 | +92 | +1.6% |

| Property Trust Index | 1174 | +49 | +4.5% |

| Utilities Index | 7474 | -179 | -2.4% |

| Financials Index | 4131 | -27 | -0.7% |

| Materials Index | 12772 | +735 | +6.1% |

Friday closing values

| Index | Change | % | |

| U.S. S&P 500 | 2855 | -8 | -0.3% |

| London’s FTSE | 5993 | +193 | +3.3% |

| Japan’s Nikkei | 20388 | +351 | +1.7% |

| Hang Seng | 22930 | -867 | -3.7% |

| China’s Shanghai | 2814 | – | – |

Key dividends

| Date | |

| Mon 25 May | Div Ex-Date – Elders (ELD) |

| Tue 26 May | N/A |

| Wed 27 May | Div Ex-Date – AMCOR (AMC) |

| Thu 28 May | N/A |

| Fri 29 May | Div Ex-Date – NABPB |

–

Monday 25 May 2020, 5pm

For more information on the above please contact Bentleys Wealth Advisors directly or on +61 2 9220 0700.

This information is general in nature and is provided by Bentleys Wealth Advisors. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decision based on this information.