Stocks continued to fall, with most indices down for the sixth week in a row. The MSCI World was down 1.8%, led by a 2.4% fall in the S&P 500 despite a big Friday rebound. If we apply the bear market definition of losses greater than 20% from the peak, the S&P 500 managed to narrowly avoid that label for now, rebounding from a drawdown of over 19% from the early January peak during the week.

The S&P/ASX 200 fared slightly better, falling 1.6% for the week, remaining one of the best performing developed markets year-to-date. Tech continued to lead declines with a 6.7% fall, while Materials were weak on worries over China’s economic growth. Healthcare (+2.6%) was the only sector in the green, despite CSL announcing that it expected delays for the Vifor acquisition to receive the necessary regulatory approvals, while Financials (-0.5%) performed well on the back of solid updates from Westpac (WBC) and Commonwealth Bank (CBA). Suncorp had a solid quarter for the bank division and rumours swirled around a potential takeover offer for the division from NAB. Elsewhere, Pendal (PDL) posted a solid first half with a boost in revenues and earnings from the TSW acquisition. Xero (XRO) reported its FY22 results that was mixed, with revenue growth remaining strong but margins and earnings disappointed as it continues to reinvest heavily into its business.

Meanwhile, bond yields fell as investors flocked to safe havens as fears that central banks would need drive economies into recession to slow inflation. The U.S. 10-year Treasury yield fell 0.2% and is back below 3%, ending the week at 2.93%. Australia’s 10-year government bond yield fell by a smaller 0.07% to end the week at 3.39%. These moves occurred despite U.S. inflation figures coming in higher than expected at 8.3% year-on-year relative to the 8.1% expected by the consensus. This may be due to the market seeing inflation as having peaked, more on this below.

Commodities were largely lower for the week as worries over the Chinese economy continue. Trade and loan growth data were both anaemic while Chinese purchasing price growth remains elevated at 8%. Together, this means that the economy remains weak while costs continue to rise. With China still a major production hub for the rest of the world, this potentially means more supply chain and cost pressures for the world.

In Australia, the NAB business survey indicated a resilient backdrop for businesses, with conditions continuing to improve, buoyed by continued reopening trends, while confidence has held steady. On the other hand, consumer pessimism deepened. The Westpac consumer sentiment survey reading fell significantly as expectations for future family finances and house prices took a dive.

This week, Australian employment data and wages will be the primary focus for domestic markets. Globally, the U.S. releases retail sales and industrial production data, Europe has its first-quarter GDP reading, and China has its monthly fixed asset investment, industrial production, retail sales and unemployment rate readings.

Inflation likely peaked but underlying trends may be more worrisome

Though a peak in U.S. year-on-year inflation may be behind us, with the latest reading falling to 8.2% from the previous 8.5%, the above-consensus core inflation reading indicates a bleaker outlook. Inflation growth can only grow higher if prices continue to rise so headline inflation may moderate as energy prices stabilise, though food inflation may have further to run.

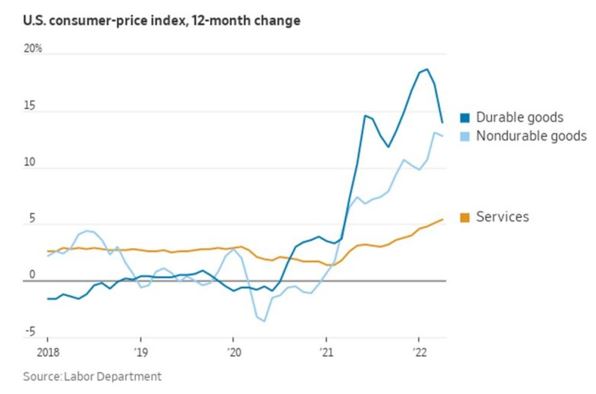

The rise in core inflation is more worrisome. The chart below shows that while durable goods (computers, cars, kitchen appliances etc.) inflation is starting to moderate, nondurable goods (paper, food, medication etc.) inflation remains elevated, and services continues to push higher.

Durable goods saw a surge in demand from the pandemic and supply constraints from lockdowns. This is now easing as pandemic restrictions are rolled back and consumers shift spending back to services which tends to be the stickier part of inflation. This means that the potential easing of supply chain issues when China emerges from its most recent round of lockdowns is unlikely to bring inflation down fast or low enough for the U.S. Federal Reserve to pivot to a more patient stance.

Furthermore, other inflationary shocks may permeate through the world as protectionism is increasing. Over the weekend, India announced that it would implement strict export controls on wheat, further exacerbating already tight global supply.

As a result, we remain cautious and maintain an underweight to risky assets as we expect further volatility ahead until there is more clarity on a pathway for inflation to moderate and for central banks to be less aggressive in hiking rates.

–

Monday 16 May 2022, 3pm

For more information on the above please contact Bentleys Wealth Advisors directly or on +61 2 9220 0700.

This information is general in nature and is provided by Bentleys Wealth Advisors. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decision based on this information.