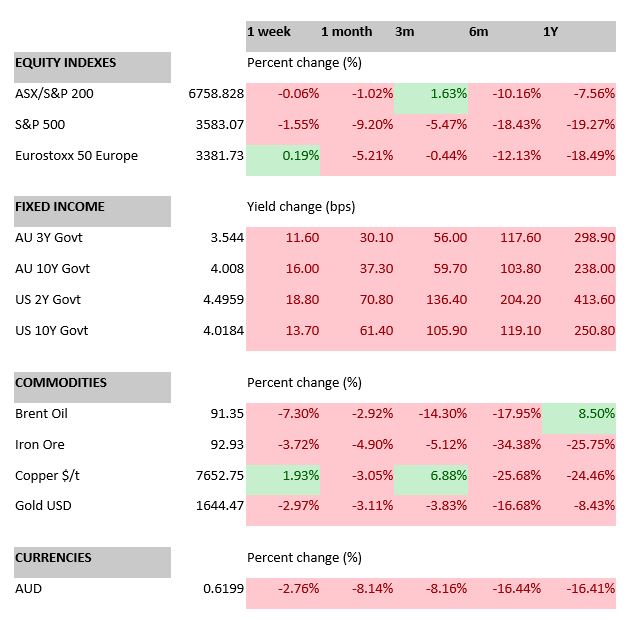

KEY ECONOMIC RELEASES LAST WEEK

- Westpac consumer sentiment fell 0.9% and remains deeply pessimistic, has not been able to build on last month’s bounce. RBA’s smaller than expected hike injected some optimism into the latter survey results which may see an improved reading next month. Expectations for economic conditions, unemployment and time to buy a dwelling all fell sharply over the month.

- NAB business survey conditions improved further but sentiment remains weak and below historical average. Cost pressures remain high but easing, forward orders and capex intentions remain supportive.

- US inflation came in above expectations again with CPI at 8.2% YoY and core at 6.6% YoY. Monthly readings were 0.4% and 0.6% respectively. This remains well above the Fed’s targets. Though forward leading indicators are showing signs that inflation should slow, this is still not coming through the hard data yet which will not deter the Fed from continuing to hike.

- US retail sales were flat MoM which indicates negative growth after accounting for inflation and a weakening consumer.

- China inflation remains muted with CPI rising 2.8% YoY. Importantly, PPI continues to trend lower, coming in at 0.9% YoY. This remains an important leading indicator for goods inflation globally and indicates that goods inflation is likely to continue to trend lower.

- China liquidity data was positive as stimulus continues to work its way through the system.

KEY RELEASES FOR THE WEEK AHEAD

- Australian employment data

- China GDP, fixed asset investment, industrial production and retail sales

- EU inflation figures

CHART OF THE WEEK

As we await the quarterly domestic inflation figures that will likely be higher than the previous reading, we note that the Reserve Bank of Australia slowed its hikes to 0.25% at the recent meeting. The monthly inflation indicator may be a factor, with the series showing a stabilisation and potential peak in the September quarter.

–

Monday 17 October 2022, 3pm

For more information on the above please contact Bentleys Wealth Advisors directly or on +61 2 9220 0700.

This information is general in nature and is provided by Bentleys Wealth Advisors. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decision based on this information.