Recession fears continue to dominate leading to another week of equity losses and bonds rebounding. The MSCI World fell 1% with the U.S. S&P 500 falling 0.9% despite a positive end to the week as the quarterly earnings season kicks off. Early results are mixed with the big U.S. banks reporting mixed results as consumer and business demand for loans remain strong while investment banking revenues have fallen off a cliff. The banks are also building reserves again in anticipation of rising bad debts in the coming months. Meanwhile, there was some reprieve for tech related names as the world’s largest semiconductor foundry, Taiwan Semiconductor, posted better than expected results while also guiding for another strong quarter, allaying fears of a cliff in semiconductor demand.

The S&P/ASX 200 fell 1.1% last week as miners came under heavy pressure with iron ore and other commodity prices tanking on the back of renewed fears of a Chinese slowdown as the bad news on the property development front seems to be never-ending. Rio Tinto (RIO) did little to help sentiment as it noted that inflation would impact underlying earnings despite a decent production report. Materials stood out with a 6.5% loss while Healthcare rose 3.5% for the week. Tech outperformed with a 0.3% gain for the week thanks to a boost from Wisetech (WTC). The company upgraded guidance for the 2022 financial year as it continues to deliver strong top-line growth, driving significant operating leverage. Elsewhere, Pendal (PDL) reported disappointing net outflows of $4.2 billion as funds under management fell to $111 billion as at the end of June. While the company noted improving trends in June, the market is likely to remain sceptical given the challenging environment.

Global bond yields were largely lower with the U.S. 10-year Treasury yield falling 0.17% to 2.93% despite headline inflation coming in above consensus at 9.1%. Shorter term yields are still on the rise as traders are now considering the prospect of a big 1% rate hike by the U.S. Federal Reserve later this month, but expectations of a recession have driven longer-term yields lower. This has resulted in the widely watched recession indicator, the 2-year Treasury yield spread over 10-year Treasury yield, turning deeply negative and signalling an imminent recession. The Australian 10-year underperformed, falling just 0.06% to 3.41% as strong employment data offset the continued weakening of consumer and business sentiment.

Last week was also a big one for Chinese economic data. GDP fell 2.6% in the second quarter, worse than consensus expectations for a 1.5% fall. Industrial production and fixed asset investment also disappointed while retail sales rebounded, providing a mixed picture for the world’s second largest economy. However, the implications are not clear as China has repeatedly reiterated its commitment to the 5.5% growth target for 2022 which could mean more stimulus in the coming months. Lending data, usually a good leading indicator for Chinese economic growth, grew strongly which is a promising sign but much will hinge on the ability to avoid major lockdowns for the rest of the year.

This week, more rate hikes are on the table with the European Central Bank expected to finally make a move. Preliminary readings of Purchasing Manager Indices (PMIs) for most major economies will also provide some insight into the global economic slowdown. Markets will also be closely scrutinising companies’ guidance as reporting season picks up.

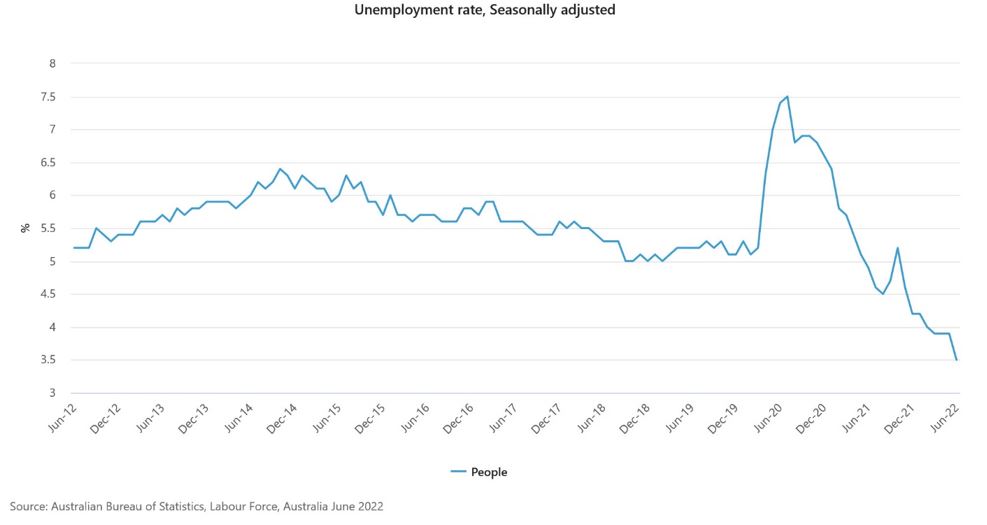

48-year lows for the unemployment rate

Another strong round of employment data has helped the unemployment rate fall to 3.5%, the lowest since 1974.

The data was unequivocally strong with 88,400 jobs added, 52,900 of those being full-time. The fall in the unemployment rate also comes at a time when the participation rate and employment to population ratio is rising, with both at the highest in the last 10 years. This highlights the current strength of the domestic economy and we remain positive on the outlook relative to other major economies. However, we would note that employment data tends to be a lagging indicator for the economy which means that while Australia is currently in good shape, it tells us little about what is to come. Other indicators are weakening, such as the consumer and business sentiment surveys released last week, which could point to a weaker jobs market in the coming months.

–

Monday 18 July 2022, 5pm

For more information on the above please contact Bentleys Wealth Advisors directly or on +61 2 9220 0700.

This information is general in nature and is provided by Bentleys Wealth Advisors. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decision based on this information.