Global equities were largely lower last week as bond yields surged. The MSCI World was 1.8% lower as the U.S. S&P 500 fell 2.2%. Emerging markets performed better, falling 1.3%, but the domestic index was once again an outperformer, up 0.6% for the week.

Utilities led with a 1.7% gain, followed by Materials (+1.6%) and Energy (+1.2%). Meanwhile, more cyclical and rate sensitive sectors such as Property (-0.9%), Tech (-0.6%) and Healthcare (-0.5%) lagged the S&P/ASX 200.

Bond yields surged as U.S. headline inflation rose 8.5% year-on-year and China’s producer prices surged 8.3%. With China still being a key manufacturing and exporting nation, the surge in producer prices is indicative of further inflationary pressures to come. The U.S. 10-year yield ended the week above 2.8% while Australia’s 10-year yield rose over 3% as a weaker than expected domestic employment report did little to deter the surge in yields. 17,900 jobs were added relative to the 40,000 expected, while the unemployment rate remained at 4%. Given the recent strength of the employment figures, the weaker reading is not yet concerning as the trend remains strong.

NAB’s business survey and Westpac’s consumer survey results were also released last week with businesses feeling more confident as trading conditions improved, especially in Western Australia as the border fully reopened in March. However, consumers did not share the same optimism as the reading fell 4.2% into pessimistic territory as expectations for economic conditions declined significantly.

Apart from producer prices, China also reported trade and liquidity figures. Exports remain strong but slowing, up 14.7% year-on-year but lower than last month’s 16.3% rise. However, imports contracted by 0.1%, a worrying sign that domestic demand has collapsed, especially given the expectations for an 8% rise. As China battles another round of lockdowns, the government has increasingly talked up supportive measures. New loan volumes and total social financing have started to rebound significantly, but it is likely not sufficient to offset the impact of lockdowns so more support will be required.

We may start to see further support in the fixed asset investment data out from China this week. Other key economic data to watch for this week are European inflation figures and preliminary results of global Purchasing Manufacturer Indices (PMIs). China also releases other key data including industrial production, retail sales and first quarter GDP, while the People’s Bank of China is also expected to provide further monetary easing.

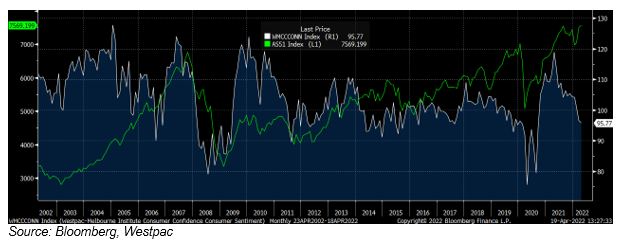

Consumers are pessimistic, should investors be?

The Westpac Consumer Sentiment is now below 100 points, the level that divides optimism from pessimism for this survey. It was last at these levels in 2020 during Melbourne’s prolonged lockdown. The survey noted inflation news being of particular concern while views on the outlook for the economy saw the sharpest falls. On the bright side, the labour market is still seen as remaining strong.

So should pessimistic consumers mean that, as investors, we should be pessimistic as well?

The white line marks the Westpac Consumer Sentiment results while the green line shows the S&P/ASX 200 index. While sentiment has coincided with some larger selloffs including the financial crisis in 2008 and COVID in 2020, the relationship between the two is largely spurious, with pessimism in 2006, 2013 and 2017 occurring during strong rallies.

While consumer sentiment is an important part of a larger group of economic indicators, it has little forecasting power for investors as other factors such as monetary and fiscal policy have more influence over market returns. A much steeper fall in the reading would be worrisome but mild consumer pessimism is not uncommon and not overly concerning for investors at this stage.

–

Tuesday 19 April 2022, 10.30am

For more information on the above please contact Bentleys Wealth Advisors directly or on +61 2 9220 0700.

This information is general in nature and is provided by Bentleys Wealth Advisors. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decision based on this information.